-

June 9, 2026

June 9, 2026 -

Comment: 0

Comment: 0

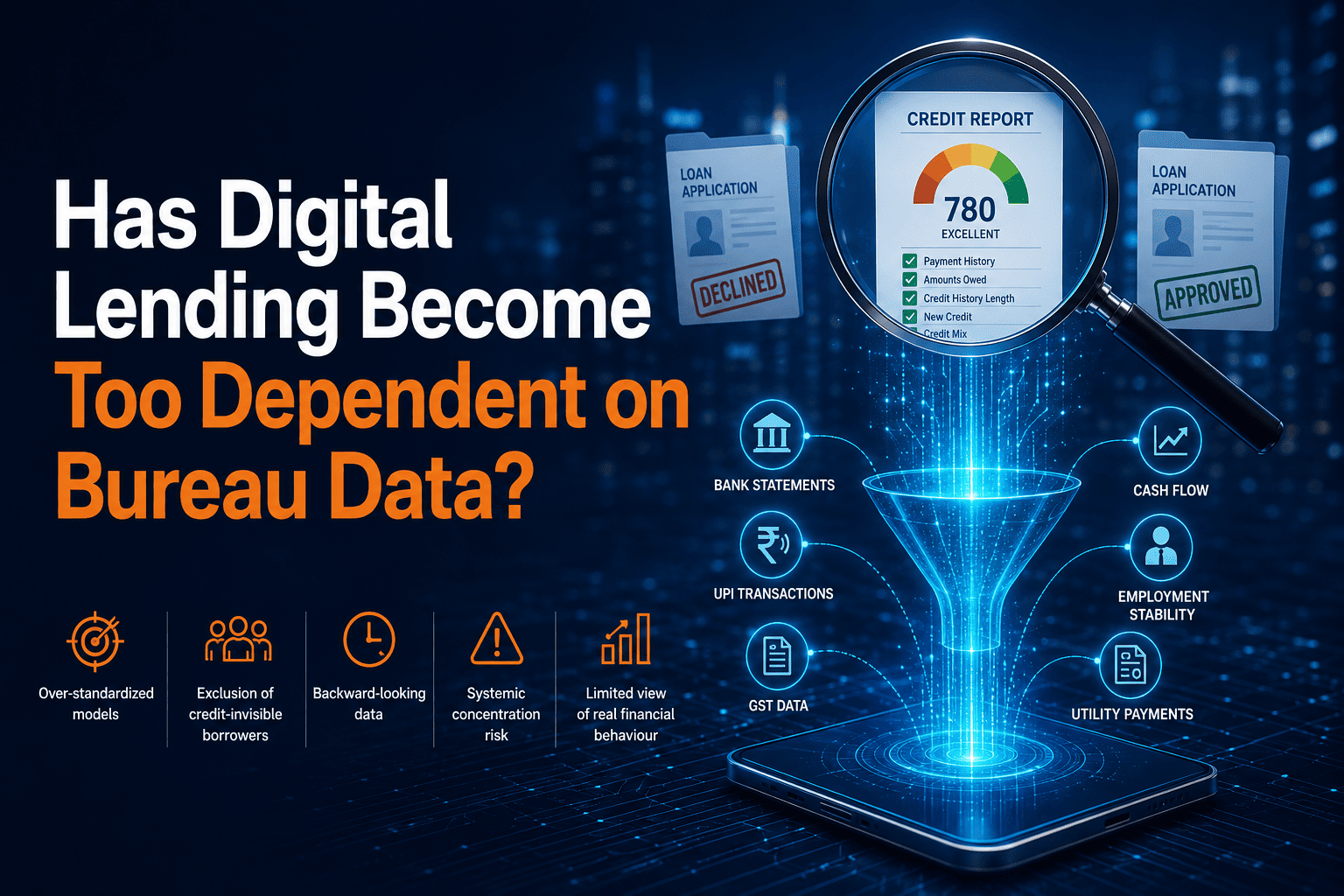

Has Digital Lending Become Too Dependent on Bureau Data

A young professional with a stable income applies for her first loan and gets rejected because she has no meaningful credit history. Meanwhile, another borrower with an excellent credit score receives loan offers from multiple lenders within days.

Both outcomes are driven by the same underlying factor: credit bureau data.

For years, bureau scores have served as the backbone of digital lending. They have enabled lenders to scale rapidly, reduce turnaround times, and improve risk management.

But as the industry becomes increasingly dependent on bureau-based underwriting, a critical question deserves attention:

Has digital lending become too reliant on a single lens of risk assessment?

As lenders continue to compete for growth while maintaining portfolio quality, excessive reliance on bureau information may be creating unintended risks for both institutions and borrowers.

The Rise of Bureau-Centric Lending

The appeal of bureau data is understandable.

It provides lenders with a standardized view of a borrower’s credit history, repayment behaviour, outstanding obligations, and delinquency patterns. Bureau-based underwriting enables quick decisions, reduces manual intervention, and supports large-scale digital lending operations.

For lenders seeking operational efficiency and portfolio control, bureau data offers a proven and easily accessible foundation for risk assessment.

However, the increasing standardization of underwriting models has introduced new challenges.

When Everyone Uses the Same Data

A growing number of lenders rely on similar bureau-driven scorecards and eligibility criteria.

As a result, underwriting models across the industry often arrive at similar conclusions regarding borrower risk. Customers with strong bureau profiles receive multiple loan offers, while those with weaker or limited credit histories are frequently declined.

This creates a market where lenders are competing for the same borrowers rather than identifying differentiated opportunities.

In such an environment, underwriting becomes less about developing proprietary risk insights and more about following a common industry benchmark.

The Credit-Invisible Challenge

One of the most significant limitations of bureau-centric lending is its inability to adequately serve credit-invisible or thin-file customers.

India still has millions of individuals who have limited formal borrowing history despite having stable incomes and responsible financial behaviour.

These may include:

· Young professionals entering the workforce

· Gig economy workers

· Self-employed individuals

· Small business owners

· First-time borrowers

When underwriting models heavily prioritize bureau scores, many potentially creditworthy borrowers remain excluded from the formal credit ecosystem.

This creates a paradox where access to credit depends on having prior access to credit.

Looking Back Instead of Looking Forward

Credit bureau reports primarily reflect historical behaviour.

While past repayment performance is an important indicator of future risk, it does not always capture a borrower’s current financial condition.

A borrower with an excellent bureau score may have recently experienced income disruption. Conversely, someone with a weaker bureau profile may have significantly improved their financial stability.

In rapidly changing economic environments, lenders must recognize that bureau data represents a snapshot of the past rather than a complete picture of present repayment capacity.

The Risk of Industry-Wide Herd Behaviour

Perhaps the most overlooked consequence of bureau over-reliance is the potential for systemic concentration risk.

When lenders evaluate borrowers using similar datasets and risk models:

· The same customer segments receive repeated credit offers

· Multiple lenders compete for identical borrowers

· Credit exposure becomes concentrated within a narrow risk pool

This phenomenon can create herd behaviour, where lenders collectively expand credit during favorable conditions and simultaneously tighten credit during periods of stress.

Such synchronized decision-making can amplify volatility across lending portfolios.

Expanding the Underwriting Lens

The future of lending is unlikely to be bureau-free, nor should it be.

Credit bureau data remains one of the most valuable tools available to lenders. However, the next evolution of underwriting lies in combining bureau insights with a broader range of financial indicators.

Emerging data sources such as:

· Bank account cash-flow analysis

· Account Aggregator frameworks

· GST transaction data

· UPI payment patterns

· Employment and income stability metrics

· Business transaction histories

can provide a more comprehensive understanding of borrower behaviour and repayment capacity.

The objective is not to replace bureau data but to reduce dependency on it.

The Way Forward

As India’s digital lending ecosystem matures, lenders will need to balance efficiency with deeper risk intelligence.

Institutions that move beyond standardized bureau-driven models and develop more holistic underwriting frameworks will be better positioned to:

· Expand financial inclusion

· Improve risk differentiation

· Identify underserved customer segments

· Build resilient lending portfolios

The most important underwriting question is no longer: “What is the borrower’s credit score?”

It is increasingly becoming: “What does the borrower’s overall financial behaviour tell us beyond the credit score?”

The answer to that question may define the next phase of innovation in digital lending.