-

May 26, 2026

May 26, 2026 -

Comment: 0

Comment: 0

Are Banks Losing the Customer Relationship to Fintech Front-ends?

A customer orders a smartphone online and selects the “Buy Now, Pay Later” option at checkout. The credit approval takes less than thirty seconds, the EMI plan is activated instantly, and the purchase is completed without any interaction with a bank branch, relationship manager, or even a bank application.

Hours later, if someone asks the customer who actually financed the purchase, there is a strong possibility the answer will be unclear. What the customer remembers is the platform experience, not the bank behind it.

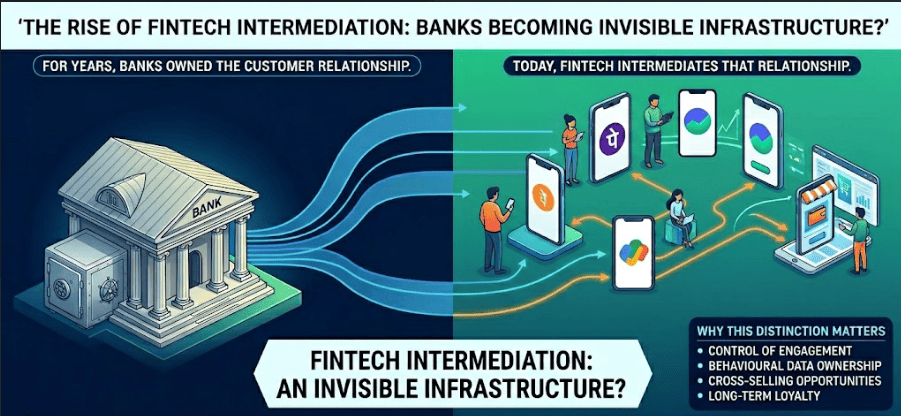

That single interaction explains one of the most important structural shifts currently underway in India’s banking and financial services industry. Traditional banks continue to provide the capital, hold the deposits, manage the regulatory burden, and carry the balance sheet risk. However, fintech platforms are increasingly controlling the customer interaction layer, which is the point where financial decisions are actually being influenced and made.

This distinction is far more important than it initially appears.

For decades, banks competed on scale, branch networks, lending capabilities, and customer trust. Today, however, the competitive battlefield has shifted toward digital engagement, customer behaviour, and interface ownership. In practical terms, the institution that customers interact with most frequently is increasingly becoming the institution that shapes financial behaviour and controls long-term customer loyalty.

At present, fintech front-ends are steadily winning that battle.

Historically, banks owned almost the entire financial journey. Customers opened accounts directly with banks, borrowed directly from banks, invested through banks, and relied on banks for financial guidance. Even when internet banking and mobile banking emerged, the relationship largely remained within the bank’s own ecosystem.

Over the last decade, that structure has changed significantly.

Today, consumers increasingly access financial services through platforms that are not traditional banks. Payments are conducted through applications such as PhonePe and Google Pay. Investments are increasingly managed through platforms such as Groww and Zerodha and other digital wealth ecosystems. Lending products are being embedded directly into e-commerce journeys, mobility platforms, merchant ecosystems, and consumer applications.

In many of these interactions, the bank itself becomes almost invisible.

This trend is not theoretical. It is visible in transaction data and customer behaviour patterns across India’s digital economy. India’s UPI ecosystem processed more than 185 billion transactions in FY25, making it the largest real-time payments infrastructure globally. However, a majority of these transactions now take place through third-party applications rather than through bank-owned digital channels.

That development has enormous strategic implications for the banking industry.

The organisation controlling the interface gains access to daily customer engagement. It captures behavioural patterns, spending habits, transaction frequency, merchant preferences, and borrowing intent. Over time, this creates opportunities to influence a much larger share of the customer’s financial life. Banks, meanwhile, risk becoming infrastructure providers operating quietly in the background while fintech platforms build stronger customer recall and engagement.

The rise of fintech front-ends is not simply a technology story. It is fundamentally a customer behaviour story.

Traditional banks were historically designed around products and operational structures. Most banking institutions still operate through separate divisions such as retail banking, mortgages, cards, wealth management, and SME lending. Fintech companies, on the other hand, are designed around customer journeys and behavioural moments.

That distinction changes how financial services are delivered.

A traditional bank often focuses on how to distribute a financial product more efficiently. A fintech platform focuses on how financial services can appear naturally within a customer’s digital activity. This explains why fintechs have integrated themselves so effectively into everyday consumer behaviour.

A customer shopping online is offered financing directly during checkout. A small business using a digital commerce platform receives working capital recommendations based on transaction history. A salaried employee receives pre-approved credit immediately after salary credits are detected.

The financial product is no longer positioned as a standalone banking service. Instead, it becomes an embedded layer within a broader digital experience. This model is changing customer expectations rapidly.

Consumers now expect onboarding to be instant, verification to be paperless, approvals to happen in real time, and servicing experiences to be seamless. Customers increasingly compare banking experiences not with other banks, but with the best consumer technology experiences available in the market.

Banks have undoubtedly improved their digital capabilities over the past decade. Many large Indian banks now offer strong mobile platforms, digital onboarding journeys, and AI-enabled servicing capabilities. However, legacy technology systems, operational complexity, and slower decision-making structures continue to limit the speed at which many traditional institutions can innovate. Fintech companies, by contrast, were built for agility from the beginning.

The biggest long-term risk for banks is not necessarily the immediate loss of transaction revenue. The more significant risk is the gradual loss of direct customer relationships.

When fintech platforms become the primary interface through which customers access financial services, banks lose opportunities for direct engagement. Over time, they may also lose visibility into customer intent, behaviour, and future financial needs.

This matters because behavioural data is becoming one of the most valuable strategic assets in financial services.

Fintech platforms increasingly understand how customers spend, save, borrow, invest, and transact in real time. This allows them to personalise recommendations, improve underwriting models, and increase cross-selling effectiveness.

Banks still possess enormous volumes of financial data, but fintech companies increasingly possess contextual behavioural data, which is often more commercially valuable in a digital economy. The long-term danger for banks is commoditisation.

If customers stop differentiating meaningfully between banks and instead choose financial services primarily on the basis of front-end experience, banks may eventually compete mainly on pricing and balance sheet efficiency. That reduces differentiation and weakens long-term profitability. However, predictions about banks becoming irrelevant are exaggerated.

Banks continue to possess structural advantages that fintech companies cannot easily replicate.

Trust remains one of the biggest advantages traditional banks hold. Banking is fundamentally a trust-driven industry, particularly during periods of economic uncertainty. Customers still rely heavily on regulated banking institutions for financial stability and security.

Banks also possess access to low-cost deposits, deep underwriting expertise, strong compliance systems, and sophisticated risk management capabilities built over decades.

Importantly, many fintech business models continue to depend heavily on banking partnerships. Digital lenders require bank funding relationships. Payment platforms depend on banking infrastructure. Embedded finance ecosystems ultimately operate on regulated financial rails provided by traditional banks.

For this reason, the future is unlikely to become a straightforward “banks versus fintechs” battle.

Instead, the industry is evolving toward a layered ecosystem in which banks provide regulated infrastructure and balance sheet strength while fintech platforms provide customer-facing experiences and digital engagement.

The strategic challenge for banks is therefore not survival.

The real challenge is remaining visible, relevant, and central to the customer relationship.

The next decade of banking in India will not be defined only by who owns the largest balance sheet or the biggest branch network. It will increasingly be defined by which institutions can combine trust, digital agility, behavioural intelligence, and seamless customer experiences into a single integrated model.

Because in modern financial services, owning the balance sheet is no longer enough.

Increasingly, the institution that owns the customer interface also owns the customer relationship.