-

April 28, 2026

April 28, 2026 -

Comment: 0

Comment: 0

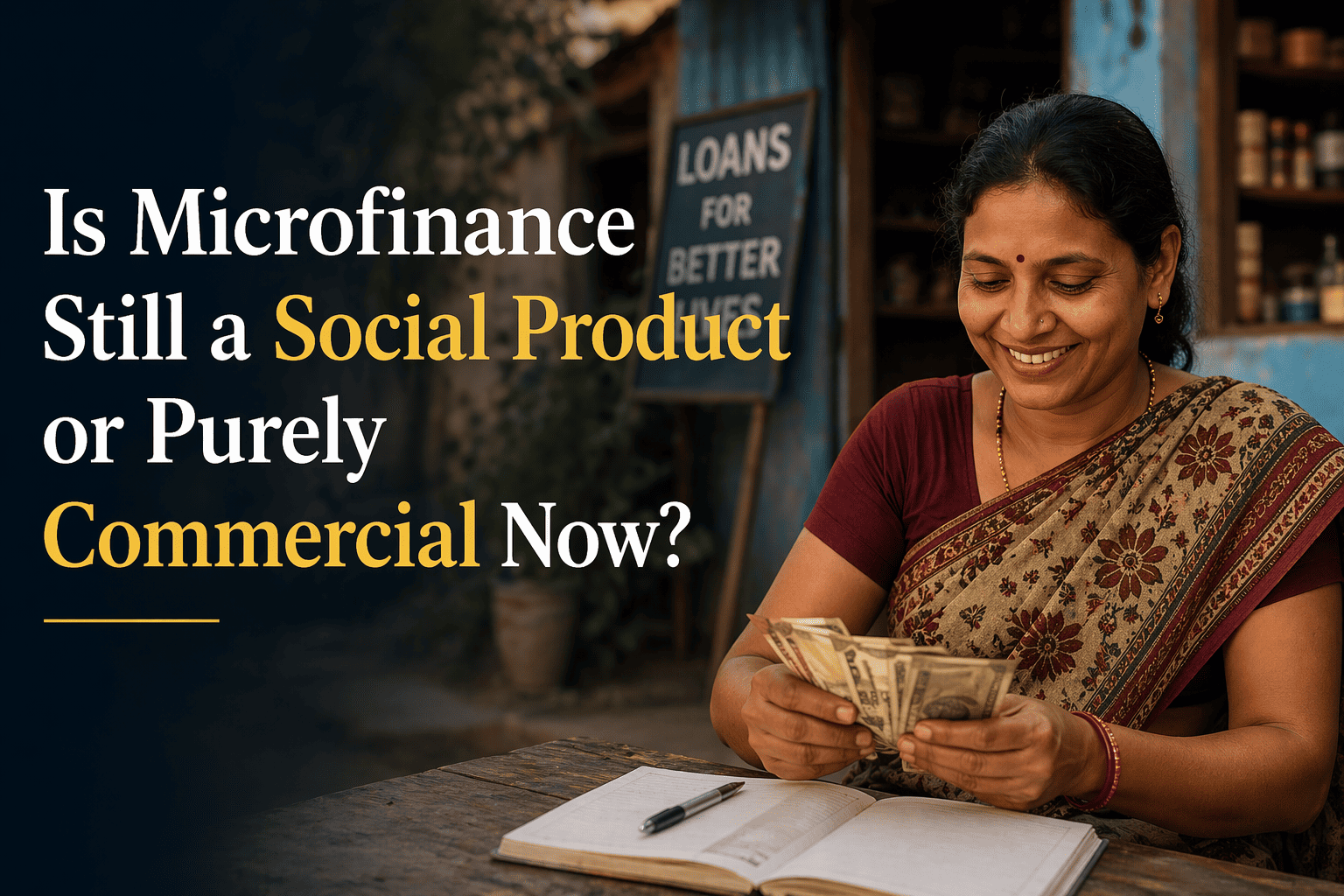

Is Microfinance Still a Social Product or Purely Commercial Now?

A Small Loan, A Big Question

Imagine a woman in rural India taking a ₹20,000 loan to start a tailoring business – no collateral, no credit history, just trust and a weekly repayment commitment. Now imagine the same sector attracting billions in institutional investment and optimizing yield like any other financial business. Has microfinance lost its soul, or simply grown up?

Purpose Before Profit And Then Scale

Microfinance was built in villages, not boardrooms. Its original mandate was simple: extend credit to those ignored by banks, displace exploitative moneylenders, and enable livelihoods, especially for women. It worked. Women still account for over 95% of MFI borrowers in India, and Joint Liability Group (JLG) models continue to rely on community trust over financial collateral.

But scale changed the equation. According to MFIN’s Micrometer report, India’s microfinance Gross Loan Portfolio grew from approximately ₹20,000 crore in FY2013 to over ₹4.33 lakh crore by Q3 FY2024, over 15x growth over the past decade. The sector now serves over 8 crore borrowers. That kind of scale attracts investors, private equity, and structured capital and, inevitably, expectations of returns.

The Uncomfortable Reality

Today’s sector asks not just “How many lives are we impacting?” but also “What’s our portfolio growth? What’s our NPA exposure?” The cracks are visible. The sector is currently navigating a significant stress cycle rising over-indebtedness in states like Uttar Pradesh, Bihar, and Tamil Nadu, and has pushed NPAs higher, with firms flagging portfolio stress in recent disclosures. The Reserve Bank of India (RBI) has sharpened its scrutiny of lending practices and borrower protection norms. This is precisely what happens when growth outpaces risk discipline.

Yet commercialization is not inherently the villain. It enabled faster expansion, better risk infrastructure, and consistent capital access. The transformation of Bandhan Bank from a rural MFI to a full-service bank with a ₹2+ lakh crore balance sheet illustrates what scale and institutional credibility can unlock. The issue is not commercialization itself. It is how far it goes before the mission becomes a footnote.

The Real Risk Is Imbalance

If microfinance becomes too commercial, borrowers become just customers, over-lending rises, and trust the foundation of the model erodes. We are seeing early signs of this in the current NPA cycle. If it swings too far the other way, capital dries up, sustainability suffers, and millions lose access to formal credit.

The RBI’s 2022 harmonized microfinance guidelines were a step toward the right balance capping borrower repayment obligations at 50% of household income and mandating pricing transparency. The institutions that treat these guardrails seriously, rather than as a compliance checkbox, are best positioned for the long run: those that track real borrower outcomes, offer financial ecosystems beyond just loans, and use data to lend better, not just more.

Final Thoughts

Microfinance is no longer purely a social product or a commercial one – it is a bridge between the two. The sector’s current stress cycle is not a sign the model is broken; it is a signal the bridge needs maintenance. How seriously institutions and regulators approach that maintenance will determine whether microfinance continues to uplift millions or becomes just another financial product in disguise. At Athena Advisors, we work with lenders to navigate this balance between purpose and performance –

strengthening credit frameworks, embedding responsible growth practices, and building portfolios that are both, resilient and